Interest Rate changes this year

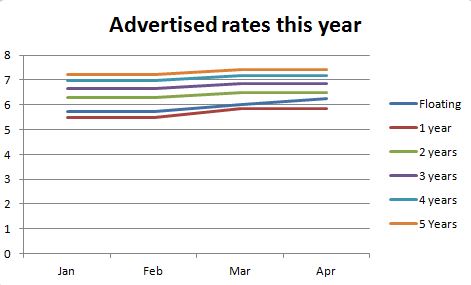

Are the rates really shooting up? Yes the Reserve Bank has had its way on the floating and short term rates, but I am not sure if the same is so true for the longer term rates. When looking at the chart below the advertised rates do all seem to have been impacted in a very tidy manner. What we don’t see so readily on these media reports are the discounts being handed to our clients after a bit of haggling.

I reckon the discounted 3 year rates I have seen coming over my desk are better than 2 months ago. Those buying with less than a 20% deposit with ANZ will also see a better interest rate today than they would have 2 months ago.

Cash incentives for new clients is still pretty much at the same levels as the previous few months. I reckon we may see a shift in better rate discounts as opposed to cash backs as consumer focus changes to the repayment figures. This would be better for existing home owners.

Cash incentives for new clients is still pretty much at the same levels as the previous few months. I reckon we may see a shift in better rate discounts as opposed to cash backs as consumer focus changes to the repayment figures. This would be better for existing home owners.

Our business has seen our client base becoming more interested in fixing for the 2 and 3 year mark. While 1 year rates still remains very popular especially now as the floating becomes more expensive.

Should you fix now?

The main reasons why people fix remains the same

1. You need to know what your payments will be

2. You feel the floating rates will get higher than the rate you are fixing for. If you fix at a rate higher than the floating now, you would need the floating rate to increase quickly enough so that you make back the extra amount you pay at the start.

To be honest fixing your rate is less about trying to make a profit than it is about ensuring that you are comfortable with the payments. The fact is that no one can predict the future and you will sometimes win on the rates and sometimes you will lose. The best advise is not to think too much about it.

Things to remember before you fix

1. You can split your loan over different fixed terms.

2. Your broker can also fix your rate

3. Usually breaking your rate will not incur a fee if rates have moved up