Interest Rate changes this year

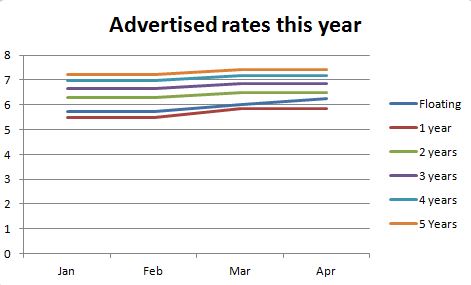

Are the rates really shooting up? Yes the Reserve Bank has had its way on the floating and short term rates, but I am not sure if the same is so true for the longer term rates. When looking at the chart below the advertised rates do all seem to have been impacted in a very tidy manner. What we don’t see so readily on these media reports are the discounts being handed to our clients after a bit of haggling.

I reckon the discounted 3 year rates I have seen coming over my desk are better than 2 months ago. Those buying with less than a 20% deposit with ANZ will also see a better interest rate today than they would have 2 months ago.

Cash incentives for new clients is still pretty much at the same levels as the previous few months. I reckon we may see a shift in better rate discounts as opposed to cash backs as consumer focus changes to the repayment figures. This would be better for existing home owners.

Cash incentives for new clients is still pretty much at the same levels as the previous few months. I reckon we may see a shift in better rate discounts as opposed to cash backs as consumer focus changes to the repayment figures. This would be better for existing home owners.

Our business has seen our client base becoming more interested in fixing for the 2 and 3 year mark. While 1 year rates still remains very popular especially now as the floating becomes more expensive.

Should you fix now?

The main reasons why people fix remains the same

1. You need to know what your payments will be

2. You feel the floating rates will get higher than the rate you are fixing for. If you fix at a rate higher than the floating now, you would need the floating rate to increase quickly enough so that you make back the extra amount you pay at the start.

To be honest fixing your rate is less about trying to make a profit than it is about ensuring that you are comfortable with the payments. The fact is that no one can predict the future and you will sometimes win on the rates and sometimes you will lose. The best advise is not to think too much about it.

Things to remember before you fix

1. You can split your loan over different fixed terms.

2. Your broker can also fix your rate

3. Usually breaking your rate will not incur a fee if rates have moved up

Reserve Bank changes

The Reserve Bank has made a few changes lately. We feel that two aspects of these changes should have an immediate impact on home buyers.

Exemptions for New Home buyers

Apart from the “Welcome Home” buyers exemption which has allowed us to approve some 90% lending to clients on regular incomes, there is now a further new exemption to help home buyers. In particular, the Reserve Bank proposes to exempt any residential mortgage lending “to finance the construction of a new residential property.” Reserve Bank Paper

What does this mean?

Under the proposal, lending with a deposit of less than 20% will be possible for clients who are constructing or buying a new home.

Who can use the new exemption?

1. Someone buying from a builder. The reasoning for this exemption is to ensure the Reserve Bank LVR restrictions do not result in less houses being built. So the buyer must make a financial and legal commitment in the form of a purchase contract before construction has begun. Payment may be made in stages or in one lump sum at the end of a project. Services could be provided to the section prior to a buyer being found.

2. Someone who is buying land and building on it. We note that at present most banks require a 20% deposit before lending for a land purchase and only a couple of banks will entertain a construction project with less than a 20% deposit. Westpac are able to look at applications with a 10% deposit for a construction project when building is to be done with a full fixed price contract. (other conditions apply)

Who cannot use the new exemption?

1. Someone seeking a loan to buy a section with no immediate plans to build.

2. Someone seeking a loan to buy a section and to move a house onto it.

Please note that banks are lending outside of these rules for certain clients, call me first if you have a specific scenario you would like to discuss.

Investors with 5 or more houses

The Reserve Bank has also made some decisions on its review of bank capital adequacy requirements for housing loans. Of importance is its decision on the number of properties a client would have with a bank, before the lending should be considered to be for “corporate property”. This may affect the cost to a bank of funding this type of a client. The RBNZ has stated that anyone with 5 or more houses should be treated as a small business owner.

We are unsure of the actual effect on pricing this will have,but note that:

– currently commercial property loans are priced anywhere from .5 -1% higher than residential property loans; and

– generally banks will lend approx 65% over a 15 year term with any amount greater than 65% placed on a shorter term.

Interest rate’s sneaky moves

There was a time when the floating interest rate was considerably higher than the fixed rates. Only five years ago the two year rate was around 8% and the floating around 10%. After many years of low interest rates, one feels, that a wait and watch approach is the best to take when it comes to considering fixing rates. And with the Reserve Bank of New Zealand issuing only a verbal warning of what may be higher interest rates in the future, many feel like they can roll over and hit the snooze button once again.

However we have noticed a particular trend developing over the past year. The floating interest rate has been unchanged but the fixed rates have started their climb upwards. The Reserve Bank has a lot of influence over our rates but since we tend to rely on raising capital from abroad quite heavily, there is a component of dependence on the global markets as well. Over the past ten years we NZer’s have paid a lot on our interest rates compared to other countries as there is particular perception of riskiness due to some of the fundamentals of our economy.

Can The Reserve Bank Relax?

Does the Reserve Bank have a good reason to try to slam the brakes on the housing market? You often read articles talking about house price increases which seem too ridiculous to fathom, but how normal is this for Auckland? Is this the start of another boom or just a little bump before a cliff? Below you will find a graph which illustrates the percentage change in house prices. It is interesting to note that it is common to have increases above the ten percent mark.  After a pretty serious financial catastrophe in 2008 we saw dramatic decreases in house prices, for almost 2 years. Now, after clambering out of the recession, we have seen some very dramatic increases in the past year, surprisingly, well before the economy has kicked into high gear.

After a pretty serious financial catastrophe in 2008 we saw dramatic decreases in house prices, for almost 2 years. Now, after clambering out of the recession, we have seen some very dramatic increases in the past year, surprisingly, well before the economy has kicked into high gear.

I guess the thing on the Reserves Banks mind would be the potential increases we might see once we actually have a buoyant and seriously confident economic backdrop. Looking a bit deeper into the increases in Auckland we find that the North Shore is heading towards becoming a serious challenger to Auckland Central. On the other hand areas previously considered to be more volatile in tough times now seem fairly stable.

The Reserve Bank’s new act of holding first home buyers at the gate may also act as a kind of insurance policy for property investors, since any dramatic slow down in the property market would be preceded by the Reserve Bank opening the flood gates; allowing investors to offload their assets. An interesting story should reveal itself over the next two months – namely the impact of the new Reserve Bank restrictions. From feedback from many real estate agents in the market, we are hearing stories of more willing vendors and a more stable pattern of purchasing moving forward. That said, we still feel that it is hardly a buyers market. With low interest rates around and secured on the horizon there is little rush to sell up. Further there is much less motivation to sell from home owners unable to trade up due to new LVR restrictions.  The talk about freeing up land is still just that; With the average subdivision usually costing more than $80k before getting a title, profits have to be well in excess of this amount before anyone pulls out a hammer. Its ok for areas where more than $150k profit can be made easily from the process. Unfortunately the bulk of the areas with a lot of land do not offer the profit margins required to make the risk worthwhile .

The talk about freeing up land is still just that; With the average subdivision usually costing more than $80k before getting a title, profits have to be well in excess of this amount before anyone pulls out a hammer. Its ok for areas where more than $150k profit can be made easily from the process. Unfortunately the bulk of the areas with a lot of land do not offer the profit margins required to make the risk worthwhile .

Using a Guarantee for your home loan

Using a guarantee can be a way to add more comfort to a home loan application. Of course there are risks associated with this method of helping with the deposit. Anyone who offers a mortgage backed guarantee stands to lose their home to a mortgagee sale should the guaranteed borrowers start to miss their home loan payments.

Some guarantees can be safer than others.

What is Equity? Equity is the difference between a mortgage and the property value. If the guarantee is to help with a deposit, it will need to be backed up by some equity. So the person giving the guarantee will have to have enough equity to cover deposits for both homes.

1. Limited Guarantee – A limited guarantee can allow a limit on the guarantee. Some banks are happy to limit the guarantee to only the required amount. So lets say a child has a 10% deposit but required only another 10%. The guarantee could then be limited to the dollar amount which would make up the ten percent. This would give a total of 20% equity for the new home.

1. Limited Guarantee – A limited guarantee can allow a limit on the guarantee. Some banks are happy to limit the guarantee to only the required amount. So lets say a child has a 10% deposit but required only another 10%. The guarantee could then be limited to the dollar amount which would make up the ten percent. This would give a total of 20% equity for the new home.

2. Unlimited Guarantee – this can mean that the guarantee is for the full home loan amount and even can cover any future borrowings of the person being guaranteed. Of course this is not the ideal type of guarantee and less preferable to the guarantor.

Another option – split loan

Another way to help a family member to purchase a home could be to borrow the amount required to make up the deposit jointly against the home with the equity. This can than be used as a deposit and the rest of the funds can borrowed against the family members names alone.

This can add another layer of safety if things were to go sour, as the house being used for the equity can be safe as long as payments are made on the joint loan. Which would be of a much smaller amount. This can allow the joint loan to be paid quicker to reduce the time that both properties are linked.

Using a joint loan can be another way to guarantee many kids. This is as the first joint loan will only use part of the equity of the home so the rest is available for other kids or family members.

Contact us today for a free one on one discussion about what might suit your needs best.

The safety of medical insurance

I have been lucky enough to have Pra as my client for many years; she has to be one of the most positive people I know. She has had to bear some hardships in the past year and she shares some of her experience with us:

Last year in March I was saddened by the death of a friend who had been battling with breast cancer for a year. After this point I was a lot more aware of my own health and a small lump prompted me to visit my doctor. It was only the size of a mosquito bite so I was not too concerned at the time, my doctor being cautious got me into to do a mammogram. I had taken medical insurance years earlier from Hamish Patel at mortgagesonline.co.nz and was able to get a biopsy done within hours of the mammogram.

The results were in within a couple of days and my husband asked me about my hurried search for the medical policy documents. It was then I told him the sad news from the doctor – they had found three aggressive tumours deep behind the initial lump. It had turned out that the lump I had found was not the major concern, the three tumours were. And unfortunately of the type that grew fast.

The next few weeks were a very sad time, my kids and my husband were even more devastated than me. Sashi at mortgagesonline helped me a lot during this time, ensuring within days that One Path had approved my entire claim for the treatments which were to follow.

Within a few weeks I was on the operating table, everything happened so quickly. I was eager to get the cancer out of my body. The three grey lumps about the size of a pea were extracted. I had great support from the team at Breast Associates and my surgeon Wayne Jones. The chemo started not long after this operation and there was a lot of stress on my body. I was in a support group with some other breast cancer sufferers going through the same experience, not all of them made it through.

Because I had caught the cancer so early, before it had any chance of spreading, my prognosis looks good. The burden of the experience was made that much easier by dealing with a supportive broker, Sashi from mortgagesonline.co.nz always kept me in the loop with the payment side of things. And taking one of the best policies in the market from One Path, ensured that 100% of the costs to date has been covered. This has amounted to more than $110,000.

I strongly feel that anyone on an average income would struggle to meet the costs for private treatment which averages to be $150,000 in total.

Will the interest rates increase?

We have had a few banks increase their fixed term rates in the past two weeks and this mainly around the 3-5 year terms. With the commentary from our Reserve Bank pointing to a low OCR till next year it is easy to understand why many of our clients are only fixing for the short term. With the economy cooling across the ditch, the Australian Reserve Bank is also keeping its rates low.

Global sentiment also plays a major part in the fixed term rates as well and we see some things on the horizon which seem to point to increases ahead. In the past few months wholesale rates have been making a move and this has been the cause for some recent upward movement in the 3 to 5 year fixed terms.

Here are some of the factors which may change things for our home loan rates.

China’s easy lending

The PBOC or People’s Bank of China (the central bank) has been making some noises about slowing down the speculative lending carried out by Chinese bankers; Mid June a quick tap of the brakes by the central bank led to a sharp increase in the costs of interbank funding temporarily. There has been much talk about the Chinese economy slowing down; at the same time the top brass is looking at ramping up the domestic consumption to wean off reliance on exports and investment. Moving to more market based rates could be one way for this to happen; potentially increasing the cost of funds.

Fed Reserve – U.S to slow down the printing press

The Federal Reserve in the U.S has been making some grumblings about slowing down how quickly it prints money, currently the press is running to the tune of 85 billion a month. Some indications are that this might happen in the following year or two; although unemployment would ideally have to fall below the 7% mark. This slow down may also have a flow on effect on the cost of borrowing abroad.

Borrowing from abroad – higher costs?

International regulators have been talking about changing how the Australian banks raise money abroad, pointing to introducing a margin on cross-currency swap deals as a way to limit excessive risk taking and reduce systemic risk. This has some major implications for the Aussie banks as around a fifth of their funding is through foreign currencies. The major banks are having a healthy talk to international regulators about the increase in the costs of borrowings, which would probably be passed on to the end consumer.

All in all there are a few things out in the horizon which seems to spell an increase in the costs from borrowing from abroad. We wonder about the implications of the Reserve Bank and its unfavourable treatment of low deposit buyers – could this mean increased competition from the banks to retain home owners with good equity and hence better rates for some? If the new changes by the Reserve Bank cool the housing market, will they need to raise the OCR so quickly? Also with some of our major trade partners slowing some signs of a slow down, short term rates could stay attractive.

Reserve Bank changes in simple terms

One of the main functions of the Reserve Bank of New Zealand is to promote actions which  help to make our financial system more stable. The new set of tools which are set out in the latest Memorandum of Understanding between the Bank and the Minister of Finance, is to assist in this.

help to make our financial system more stable. The new set of tools which are set out in the latest Memorandum of Understanding between the Bank and the Minister of Finance, is to assist in this.

The main goal is to minimise the impact of any sudden changes to supply of money in the banks and any sudden changes to asset prices. Obviously there are still some wounds from the last Global Financial Crises around the globe and these changes may help us in the next one.

Of the four main instruments; the restrictions on high LVR lending is quite interesting.

Restrictions on high LVR lending

Note that these tools are not in place to contain house prices in Auckland and Christchurch, they are there to assist towards greater stability in the financial system.

“Quantitative restrictions on the share of new high loan-to-value ratio (LVR) loans to the residential property sector. These include:

– Restrictions on the share of new high LVR lending that banks may undertake

– Outright limits on the proportion of the value of the residential property that can be borrowed to create a minimum equity buffer for the lender” (Reserve Bank)

The Reserve Bank will give at least two weeks notice before they use this tool.

The possible impact

If this instrument was used by the Reserve Bank it could mean less borrowers with a low deposit are able to buy. It could also mean that a borrower with a smaller deposit could pay more to get the mortgage. The days of a second mortgage could return with more opportunities for finance companies to assist in bridging the gap between the bank and the purchase price.

I also think that if this type of restriction was in place for a while there could be additional pressure for the banks to promote other types of loans to continue to grow their books. Low Doc lending could be one example of this.

Countercyclical capital buffer

“The countercyclical capital buffer (CCB) framework is an additional capital requirement that may be applied in times when Excess private sector credit growth is judged to be leading to a build-up of system wide risk.”(Reserve Bank)

Basically the banks could be asked to increase the amount of capital they have to hold when the market gets busy which could be later released when the market slows down.

The Reserve Bank will give at least 12 months notice before they use this tool.

The possible impact

This could mean a greater competition for capital and again an increase in the cost of borrowing. This could impact the cost for all borrowers.

This could help in a downturn as the bank would be able to reverse any requirements and in turn promote lending.

Adjustments to the core funding ratio

“The baseline core funding ratio requires bank to source at least 75% of their funding from retail deposits, long-term wholesale funding or capital.

A CFR tightening would increase system resilience by increasing the use of stable funding and could also lean against the credit cycle”

Basically this will give the Reserve Bank the ability to increase or decrease the amount banks must hold as retails deposits, long term wholesale funding or capital.

The Reserve Bank will give at least 6 months notice before they use this tool.

The possible impact

The tightening in this could later be loosened to enable banks to maintain a flow of credit when there is a significant deterioration in external funding market conditions. This could mean better returns for term deposit holders during those times that the bank sees fit to increase this requirement.

Sectoral capital requirements

“Adjustments to sectoral capital requirements would require banks to hold extra capital against a specific sector or segment in which private sector credit growth is judged to be leading to a build-up of system-wide risk.

The Reserve Bank will give at least 3 months notice before they use this tool.

The possible impact

The intention of this tool could be great to contain certain markets while not hindering the borrowing to another. Such as cooling affect on the housing market while farm lending continues.

Increase in costs would be likely for the certain sector but banks could choose to pass the costs of holding this extra capital to other sectors.

Interesting instrument and is used for a longer period may create asset bubbles in certain sectors.

The Draft Unitary Plan

Looks like home owners will be able to build more dwellings per site depending on the specific new rules for zones.

| Zone | Dwellings |

| Single House | One dwelling per site |

| Mixed Housing | One dwelling per 300m² net site area where up to four dwellings are proposedNo density limits apply where five or more dwellings are proposed and the requirements of clause 4.3.1.3.1.2.a and b are met |

| Large Lot | One dwelling per site |

| Rural and coastal settlements | One dwelling per 4000m² net site area |

There is a tool for viewing the new zones(check out your property) here

the key for the map is here

Will your mortgage repayment insurance help?

This month our in house Insurance Broker -Vijay Singh writes about three things you should check on your mortgage repayment cover:

This month our in house Insurance Broker -Vijay Singh writes about three things you should check on your mortgage repayment cover:

1. How long will your policy pay out for? We are surprised at how many people add on a policy to their home loan which pays out for a 6 month term and think they will be covered for a lot longer. The payment term stipulates how long you can claim for and we recommend a payment term till age 65, so that clients are not forced to sell their home.

2. What happens if you change banks? Some covers are linked to the bank you are with, which may seem fine when you start. But what about years from now when another bank offers you a much better interest rate? Will you be able to move your insurance?

Well usually this is not a problem but if your health has changed, full mortgage repayment cover might not be possible.We always recommend taking a cover independent of the lender so that you are able to keep the cover regardless of who the home loan is with. These days covers are available which also automatically change to an income cover after you have paid off your mortgage.

3. Did you read what you had signed, many health questions get overlooked when taking a policy. This can cause serious issues if and when you claim. Non disclosure is one of the leading reasons for not paying a claim. Basically this is when the insurance provider says; thank you for all your premiums for those many years but you forgot to mention certain health issues when you had signed the application form, so we cant pay your claim – in fact we may even cancel all your policies.

We recommend that when you take your policy – read what you are signing for and answer all the health questions carefully. We always go through a thorough health questionnaire to ensure we set up a safe usable policy.

Call us today to book a no obligation review of your covers on 09 625 4693.